There will be many lessons to learn and conclusions to be made over the Silicon Valley Bank (SVB) fallout, but what we know is that SVB rapidly grew during the pandemic. In 2021 SVB’s deposits grew from $62 billion to $124 billion, in part due to the fact that SVB offered higher rates on deposits than many of its larger rivals.

To help fund these higher rates, SVB kept lower levels of deposits than other banks on hand and invested significant capital in startup company loans and higher-yield bonds. But that strategy failed when the Fed began hiking rates, and the venture capital market began to experience instability. This combination of higher rates and a slowdown in tech was a one- two punch for SVB.

The value of the bank’s investments shrank, and previously cash-heavy depositors started withdrawing cash deposits to fund operations.

SVB played an important role in the startup ecosystem. Without it, financing for startups is likely to become more difficult and more expensive; and this may lead to further instability in venture capital markets, an increase in loan defaults, and further declines in the value of SVB’s investments. In the event of default, the proper securitization of intellectual property (IP) pledged as collateral will be critical to the recovery of portfolio value.

The failure of SVB is a cautionary tale and a good segue into a discussion of patents as debt collateral and the importance of perfecting security interests.

As the economy continues to evolve away from traditional manufacturing to knowledge and services, so has the focus of enterprise capital investment. Historically, enterprise investment was focused on the tangible assets and infrastructure needed to maintain and grow operations. Today, however, investment is focused on technology, innovation, and knowledge-based assets; and this IP investment plays a fundamental role in the creation of corporate value. IP is a dynamic corporate asset, acting as a driver of revenue, a signal to investors, and collateral for businesses seeking to borrow money.

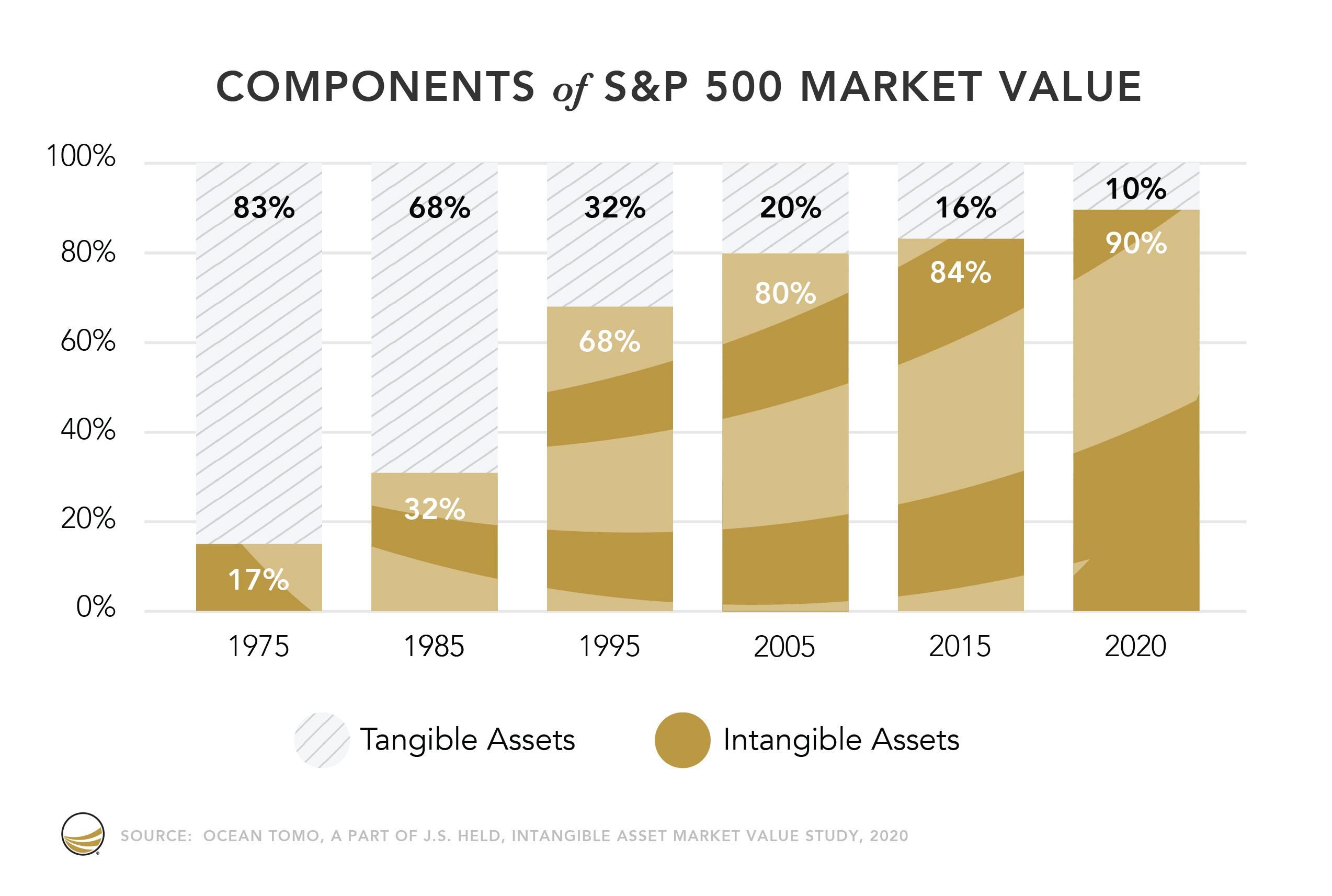

As of the date of this article, the United States Patent & Trademark Office (USPTO) has recorded more than 62,000 patent assignments where patents were pledged as debt collateral. Moreover, looking as far back as 2013, more than 40% of firms with patents outstanding had, at some time, pledged their patents as collateral. Historically, patents were pledged alongside other assets, but the tide has shifted, and lenders’ perspectives on the benefits of taking patents as collateral have improved dramatically. This change in perspective is due to several factors. First and foremost is the evolution of the U.S. economy. Over the last fifty years, the US economy has shifted from a manufacturing economy to a knowledge-based economy. In a knowledge-based economy, value creation and competitive advantage are driven by technological innovation. In a knowledge-based economy, IP is a company’s most valuable asset, and tangible assets take the back seat. The growing contribution of IP to corporate value is clear. As shown below, the value of intangible assets as a percent of market value has grown from 17% in 1975 to 90% in 2020.

In addition to the growth in value attributable to IP and patents, there has been a broad increase in the number of IP and patent transactions. These transactions, cross-licenses, and acquisitions by patent aggregators and non-practicing entities (NPE) are indicators of asset liquidity, and this liquidity has stimulated lender interest in IP and patents as collateral.

The combination of increasing liquidity and value to corporate borrowers has been key to the growing acceptance of IP and patents as collateral. As discussed by Henry, S., Ferraro, H. and Keeton, H. “Securing a Loan with Patents, Trademarks, and Copyrights is Best for Lenders,” in Pratt’s Journal of Bankruptcy Law, Issue 1, January 2010, pp. 50-64, in a typical agreement, a third-party lender takes an interest in the patent or application to secure payment on a loan. The lender, as a secured creditor, has preferential rights in the disposition of the asset upon any default. Thus, legal ownership does not change unless and until the borrower defaults and the lender forecloses on and seizes the patent or application.

Not every patent is suitable as collateral. Patents are suitable collateral for loans when they are valuable assets that can be sold or licensed to generate income. However, there are risks associated with using patents as collateral, as the value of a patent can be uncertain and may depend on a number of factors, such as the strength of the patent, the market demand for the technology, and the availability of competing technologies. Failure to understand the value of a patent or patent portfolio may result in a significant shortage of collateral.

Perfecting a security interest in a patent means taking certain steps to protect your rights as a lender or creditor in the event that the borrower defaults on their loan or other obligation. Perfecting a security interest allows you to have a legal claim to the patent as collateral in the event that the borrower fails to meet their obligations.

The process of perfecting a security interest involves identifying the patent or patents being used as collateral, executing a written security agreement, and filing a financing statement with the relevant public office. By following these steps, you are creating a public record of your security interest, which establishes your priority over other creditors in the event that the borrower defaults.

In the United States, the process for perfecting a security interest in a patent involves:

Identifying the collateral: You must accurately identify the patent or patents that are being used as collateral. This may include the patent number, the title of the invention, and the date of issuance.

Executing a security agreement: You and the borrower must execute a written security agreement that specifies the terms of the loan or obligation and provides a description of the collateral. The UCC states that a sufficient description “reasonably identifies what is described.” The security agreement must be authenticated or signed by the debtor.

Filing a financing statement: To perfect your security interest in the patent, you must file a financing statement with the relevant office. In the United States, this is done through a public office, generally the Secretary of State. The financing statement must include the name of the debtor, the name of the secured party, and an indication of the collateral. Ideally, patent number and title will be included in the indication, but generic descriptions, for example, “all assets of the debtor now owned or hereafter acquired or arising,” are sufficient.

Filing evidence of the security interest with the USPTO. According to the statutory notice requirements under 35 U.S. Code § 261, An interest that constitutes an assignment, grant, or conveyance shall be void as against any subsequent purchaser or mortgagee for valuable consideration, without notice, unless it is recorded in the Patent and Trademark Office within three months from its date or prior to the date of such subsequent purchase or mortgage.

Searching for other security interests: It is important to search for any other security interests that may have been filed against the patent to ensure that your security interest is properly perfected and that you have priority over any other creditors.

Perfecting a security interest is critical to protecting your rights as a lender or creditor and ensures that you are able to recover your investment if the borrower fails to meet their obligations. Without a perfected security interest, you may have difficulty enforcing your rights and recovering your investment in the event of default.